|

|

Journal of Contemporary Urban Affairs

|

|

2022, Volume 6, Number 2, pages 249–263

Original scientific paper

Exploring the Nexus between Political Risk and Financial Risk in the Balkan Countries: A Wavelet-Based NARDL Coherency analysis

*1 Dr. Sadat Momoh Shuaibu , 2 Assoc. Prof. Dr. Dervis Kirikkaleli

1 & 2 Department of Banking and Finance, Faculty of Economics and Administrative Sciences, European University of Lefke, Northern Cyprus

1 E-mail: ssmomoh123@gmail.com , 2 E-mail: dkirikkaleli@eul.edu.tr

|

|

ARTICLE INFO:

Received: 25 August 2022

Revised: 18 October 2022

Accepted: 19 November 2022

Available online: 24 November 2022

Keywords:

Political risk;

Financial risk;

Wavelet analysis;

NARDL coherency analysis;

Balkan countries;

Urban planning;

Inclusive growth.

|

ABSTRACT

The empirical investigation of which risk factor—political or financial—is the optimal driver of country risk in emerging economies in the twenty-first century has grown into a significant and volatile issue in recent decades. This paper investigates the linkages between political risk and financial risk in four Balkan economies (i.e., Greece, Albania, Bulgaria, and Romania) from 1984 Q3 to 2018 Q4, using non-linear autoregressive distributed lag co-integration (NARDL) and wavelet coherence approaches. As a result, findings from the links between political risk and financial risk are being used to provide significant insights into effective urban planning in Balkan cities. The outcomes of the NARDAL analysis indicate that there are short-term and long-term asymmetric links between political risk and financial risk in the Balkan countries except for Romania. The wavelet coherence study also revealed that there is significant vulnerability between political risk and financial risk at different frequencies in the region, also, political risk is a key for predicting financial risk over the selected study period at different frequencies in Albania and Bulgaria.

|

|

|

|

This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution 4.0 International (CC BY 4.0)

Publisher’s Note:

Journal of Contemporary Urban Affairs stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.

|

|

JOURNAL OF CONTEMPORARY URBAN AFFAIRS (2022), 6(2), 249-263.

https://doi.org/10.25034/ijcua.2022.v6n2-10

www.ijcua.com

Copyright © 2022 by Shuaibu, S. M., & Kirikkaleli, D.

|

|

|

|

1. Introduction

Country risk is an ancient global problem, while contagious diseases and cyber-attacks are considerably more recent occurrences threatening the world's economies. Regardless of how well-structured a nation's economy is, there is a chance that risk elements will exist (Hacker, 2019). Some risk factors can appear suddenly, while others might develop due to laws or regulations. Studies in recent years have indicated that factors related to bad governance, particularly after the 2008 global financial crisis, are linked to the fall of governing institutions, particularly in emerging economies (Humphrey & Michaelowa, 2019).

The dynamic relationship between political risk (PR) and financial risk (FR) is one of the issues that are mostly discussed in the macroeconomic literature. However, the methodology shows that the relation

between PR and FR is unclear, especially concerning the direction of causality. Political factors are seen as a volatile source of financial stability. Although studies such as Barro (1991), Białkowski et al. (2008), Chan & John Wei (1996), Charfeddine & al Refai, (2019); Cutler et al., (1988); Hillier & Longan, (2019); Kirikkaleli, (2016), (2020); Li & Born, (2006); Pantzalis et al., (2000); Pástor & Veronesi, (2013) and Smales, (2015), were the papers that examined the linkages between political risk and financial risk. However, the findings are inconclusive. Studies by (Białkowski et al. (2008), Delavallade (2006), Pástor & Veronesi (2013), and Smales (2015) argue that political risk harms financial stability. Contrary to these findings, Cassette & Farvaque, (2014); Gyöngyösi & Verner, (2022) expressed that financial risk negatively influences political risk.

Unfortunately, most of the trending events in the Balkan countries are yet to be highlighted in the economics literature. Hence, the main aim of this research is to fill this gap by employing the NARDL and wavelet coherence techniques to examine the linkages between political risk and financial risk. Thus, using these modern econometric techniques, this paper's other contribution is to proffer answers to the following questions: (i) Is there a causal link between PR and FR in the Balkan countries? (ii) If yes, what is the direction of causality? (iii) Also employ the findings to explain urban planning in the Balkan countries.

To examine the linkage between PR and FR, we used the econometric tools of NARDL and wavelet coherence. The mother wavelet (t), which contains useful tools for determining both the short- and long-term correlations between political risk and financial risk, theoretically serves as the time-frequency domain (Bredin et al., 2015). As a result, it takes the time and frequency dimensions into account simultaneously. Although out-of-sample Granger causality analysis has been used in prior studies, its contribution to the literature remains unclear (Dees & Brinca, 2013) due to systemic alterations in the interplay concerning parameter uncertainty. In order to measure the sensitivity of the link between variables in the plot, we employed wavelet coherence, which allows us to comprehend the degree of interdependence within the analysis. The study's most significant contribution is its recommendation of an inclusive growth conceptual framework to lower PR and FR in the Balkan countries in particular and the world in general. The study will also recommend effective urban planning development to urban planners based on the political-financial risk outcomes. Finally, while previous research has yielded conflicting results, the new study's conclusions will be helpful to policymakers and allow for additional debate among those working to reduce risk and advance urbanization.

The average public debt-to-GDP ratio for the Balkan region is 46.4%, while that for Central Africa is 42.2%. Nevertheless, there are considerable differences between nations. In the case of Albania, the far-right or extreme right-wing has posed a significant threat to the country's financial system as a group of people who believe to be superior to the vast majority based on racial, ethnic, and religious criteria and regard others as inferior. Since 1991, when Albania was the least developed and most isolated nation in the Balkans, the country has been dependent on assistance from foreign organizations despite not yet being a member of the European Union. Corruption in Albania has increased over the years, as evidenced by the pyramid crisis in Albania caused by political institutions. The extractive political institutions are said to have started the scheme and utilized the proceeds for personal gain. Markets can efficiently create wealth when supported by robust governmental institutions. Therefore, the small, undeveloped economy was largely shielded from the global financial collapse during the world's financial meltdown. The global financial crisis did not affect Albanian financial markets but also on the resilience of Albanian banks because the markets were less developed and no institutions filed for bankruptcy during this crisis (Suraj, 2015).

Political instability caused by communist rule imposed on the people of Albania also impacted rural-urban migration, which cumulated in the early phases of urban growth (Lerch, 2014). Difficulties faced by the Albanian government in adopting a democratic system and free market economy have made urban planning in Albania rather static. The Communists imposed restrictions on leaving the countryside in Albania between 1960 and 1990, which resulted in economic transformation as a major driver of urban transition. Furthermore, the post-communist era saw a sharp increase in urban expansion, impacting urban labor markets (Pojani, 2009). The labor market situation has worsened in Tirana, the capital city, as more than 25% of the population revealed the rapid rate of urbanization.

In 1999, Romania was experiencing its worst economic crisis due to several factors, including the nation's declining GDP, high current account deficit, inability to obtain credit, failure to pay off foreign debt, and the long-term cause of a lack of swift structural reform implementation. The country's apparent political instability was in the background of all of this (Hord, 2001). Nevertheless, the nation started its transition in 1990 with the advantages of not having any external debt and inhabitants who were enthusiastic about the end of communism. Moreso, Romania's urbanization level is far below the 52% target set by the European Union (EU) due to changes in the political system despite the declaration of new towns in 2002. Before 1989, there was socialist industrialization with a primary focus on developing industrial centers. Resulting in nationalizing residential buildings and eliminating the market's role in forming city structures (József, 2006).

Greece's situation was very different; being the tenth country to join the EU, it smoothly transitioned from a highly authoritarian to a liberal one. It was regarded as a model democracy that allowed a pluralist system. Due to the quality and capacity to guarantee rapid economic growth while engaging in borrowing, the fierce policy reforms carried out by its administration and its linkages to the EU recognized it future potential. However, the 2008 financial meltdown and the crisis brought on by the sovereign debt had a terrible impact on the country's financial and political systems. Beginning with its failure to pay its debt, which prompted the IMF's intervention and financing of the country's application for austerity measures and the government debt- to-GDP ratio increased from 109% in 2008 to 146% in 2010. On the political front, the nation faces instability that resulted in the downfall of the one-party system in favor of a multi-party system. In addition, institutional quality, corruption, and bureaucratic quality are significant obstacles to the nation's politics and economy (Butkiewicz & Yanikkaya, 2006).

It is widely acknowledged that financial stability can lead to the stable growth of a nation (Ozil, 2018). Frequent policy reforms could reduce financial risk; as a result, political risk causes the need for short-term macroeconomic policies. In addition, Pantzalis et al., (2000) examined the range of asset values in equity markets across a two-week election period for 33 different countries, and the results showed that stock prices rose within two weeks during the election. A similar conclusion was reached by Cutler et al. (1988) in their study, which found that political risk had an immediate negative effect on the US financial system. Pástor & Veronesi (2013) argued that changes in the Australian financial market negatively impacted political risk in Austria, while the Australian federal political elections, according to Smales (2015), harmed the financial market, which is consistent with Pástor & Veronesi (2013) findings. Political risk's impact on financial markets was also studied by Białkowski et al., (2008) in 27 OECD nations, and the results showed a favorable impact. Also, according to Ashraf & Prentice (2019), political strikes and labor unrest in Bangladesh harm 33 major production firms. Other studies, including Kirikkaleli, (2016) and Arcand et al., (2015), have highlighted the relationship between PR and FR in terms of economic risk.

More so, the impact of PR on FR is also seen in other empirical studies such as Mauro (1998), which utilizes OLS regression to investigate the effect of corruption on financial stability in 100 nations. The results demonstrate that corruption lowers government health sector spending, increasing public debt. After noticing this link in a survey of 64 nations using the 3SLS estimate from 1996 to 2001, Delavallade (2006) corroborated this viewpoint. Similarly, González-Fernández & González-Velasco, (2014) found that political risk due to corruption increased financial risk due to high public debt throughout the period 2000–2012 after investigating the Spanish autonomous communities. Additionally, left-wing governments are more likely to impose restrictions on capital flight than right-wing governments (Alesina & Tabellini, 1989). Therefore, elections or regime changes can affect exchange rate policies, considering their importance to investors concerning capital flight. This negative impact of political risk on financial risk was also confirmed by Siokis & Kapopoulos (2003) after investigating the impact of election cycles on the Greece exchange rates market using an E- GARCH model. Therefore, determining a suitable exchange rate depends on the government's political condition. Berdiev et al. (2012) conducted a panel investigation on the relationship between PR and FR in 180 countries using a data set spanning from 1974 to 2004. The results demonstrate that left-wing governments and democratic institutions determine the likelihood of choosing a flexible rate regime.

In addition, there has been limited study on the connection between populism and financial crisis. According to Funke et al. (2016)'s investigation into the financial crisis and its electoral consequences for 20 developed countries, far-right party vote shares increased by about 4% or 30%. However, no far-left party vote shares increased, and the outcome was statistically stronger for post-World War II periods. The study of Gyöngyösi & Verner (2022) research describes how the far-right Jobbik party in Hungary rose to prominence amid the 2008 global financial meltdown. Several Hungarian families that had taken out loans in the Swiss franc (or other foreign currencies) were severely harmed by the steep devaluation of the Hungarian forint. The study by Cassette and Farvaque (2014) revealed the detrimental impact of financial risk on political stability. They stated that debts accumulated by incumbents before elections increase their likelihood of being reelected. They also added an increase of about 20% in the vote of the far-right populists, particularly in areas where the exposure to foreign currency debt was higher.

Just as political and financial risk affects every facet of life, it also harms urban planning by migrating people, companies, and investments between cities or regions. The 2008 global financial crisis and political swings in policies have undermined meaningful sets of guidance, investment, and policies in urban statutory planning and design. It can be stated that the built environment set up by the Commission for Architecture and the Built Environment (CABE) has dissolved since 2011 due to unstable political and financial situations (Roberts & Townshend, 2017). The field of urban planning in Albania has been quite static. The uncontrolled movement of people caused by political instability, primarily towards Tirana, corrupts the urban planning system.

Given that no study has focused on political and financial risks in these countries using the wavelet coherence technique and a nonlinear autoregressive distributed lag co-integration model, this paper set out to fill this gap. Hence, the remainder of this study is organized as follows: Section 2 provides the dataset source and methodologies used in analyzing the data. Section 3 includes a discussion and empirical results, and Section 4 presents a conclusion, policy recommendations, and an important future research direction.

2. Data Sources and Methodology

2.1. Data Sources

This study analyzed the relationship between PR and FR using the International Country Risk Guide (ICRG) data from the Political Risk Service Group for Albania, Romania, Bulgaria, and Greece from 1984 Q3 to 2018 Q4. In the ICRG, the PRS group has published political, economic, and financial data for 146 countries since 1984. A country's political risk is evaluated by six subcomponents, while its financial risk is evaluated by 5. Financial risk sub-components include exchange rate volatility, foreign debt as a percentage of GDP, current account as a percentage of exports, net international liquidity, and foreign debt service. In addition, there are six sub-components of political risk: external conflicts, corruption, religious involvement in politics, law and order, ethnic tensions, bureaucracy quality, and democracy (Howell, 2011). In addition, Stata and R-software tools are used to analyze the NARDL co-integration and wavelet, respectively. Table 1 presents the summary of the descriptive statistics of this study and it indicates that there are no outliers in the datasets.

Table 1: Summary of Descriptive Statistics.

|

Period: 1984Q3 - 2018Q4

|

|

Source: Political Risk Group (PRS)

|

|

|

PRRO

|

PRGR

|

PRBU

|

PRAL

|

FRRO

|

FRGR

|

FRBU

|

FRAL

|

|

Mean

|

65.18

|

70.90

|

69.38

|

63.90

|

29.44

|

31.84

|

31.82

|

27.30

|

|

Median

|

68.00

|

71.58

|

69.33

|

65.00

|

31.92

|

32.17

|

32.83

|

33.00

|

|

Maximum

|

78.00

|

84.00

|

77.00

|

69.67

|

42.50

|

37.00

|

41.00

|

46.17

|

|

Minimum

|

45.00

|

58.00

|

61.67

|

49.67

|

15.67

|

26.67

|

15.00

|

9.00

|

|

Std. Dev.

|

8.10

|

6.90

|

3.64

|

4.53

|

7.86

|

2.75

|

6.20

|

11.33

|

|

Skewness

|

-1.10

|

-0.17

|

-0.04

|

-1.32

|

-0.11

|

-0.01

|

-0.69

|

-0.45

|

|

Kurtosis

|

3.22

|

1.92

|

2.26

|

4.21

|

1.42

|

1.67

|

2.71

|

1.55

|

|

Jarque-Bera

|

28.36

|

7.33

|

3.18

|

48.26

|

14.69

|

10.19

|

11.54

|

16.76

|

|

Probability

|

0.00

|

0.03

|

0.20

|

0.00

|

0.00

|

0.01

|

0.00

|

0.00

|

|

bservations

|

138

|

138

|

138

|

138

|

138

|

138

|

138

|

138

|

|

|

|

|

|

|

|

|

|

|

Note: PRRO: political risk in Romania, PRGR: political risk in Greece, PRBU: political risk in Bulgaria, PRAL: political risk in Albania, and FRRO: financial risk in Romania, FRGR: financial risk in Greece, FRBU: financial risk in Bulgaria, and FRAL: financial risk in Albania.

2.2. Models Estimations

2.2.1. Unit Root Test

The initial estimation step in this study is to prevent spurious regression. In a recent study, some studies have criticized the analysis of unit root tests of time series data without structural breaks (Humphrey & Michaelowa, 2019; Ashraf & Prentice, 2019; Roberts & Townshend, 2017). The study employs the unit root test of Zivot & Andrews (2002) with a single structural breakpoint analysis and this primary step is important to know if the variables employed in this study are integrated at I (1) or I(0) but not at I(2) or higher. To estimate the unit roots for Zivot & Andrews with breaks point, the mathematical null hypothesis of the unit root is formulated as:

Where xt refers to interest variables; μ is the constant term, and et is the error term. By taking unit differencing, the equation becomes Δxt = μ+ et; where Δ=(1−B); ρ is the parameter slopes for lagged variables; which becomes 1 if there is a unit root or the variable is not stationary (Zivot & Andrews, 2002). The alternative units’ roots such as ADF and FADF with a break points are criticized (Humphrey & Michaelowa, 2019; Ashraf & Prentice, 2019) and are not used for this study.

2.2.2. NARDL bounds test

The study used the NARDL bounds test developed by Shin et al. (2014). This test helps to capture the long- and short-run asymmetric co-integration relationship between political risk and financial risk. Furthermore, this technique can be employed whether the repressors are stationary at first difference or level; however, they cannot take on regressors that are stationary at I (2). The econometric models are presented below in equations (2) and (3).

(2)

(2)

(3)

(3)

The study illustrates separate estimation models for NARDL models in the following estimation equation shown below:

(4)

(4)

The fifth equation models asymmetric co-integration in the nonlinear framework association of the Balkan countries’ PR and FR. The equation also indicates the partial sums of the negative and positive changes in financial risk. Finally, as shown in equation (6), we convert conventional ARDL to NARDL.

Where p and t are lag orders estimates the short-run effects of financial risk increases in political risk and

estimates the short-run effects of financial risk increases in political risk and  measures the short-run impact of financial risk reduction on political risk.

measures the short-run impact of financial risk reduction on political risk.

2.2.3. The Wavelet Approach

The paper examines the linkage between PR and FR and follows the wavelet mathematical application postulated by (Goupillaud et al., 1984). This wavelet technique's innovation is that it decomposes a single time series into a bi-dimensional time-frequency domain. The mother wavelet's equation is shown below.

, p(t), t=1, 2, 3…., T, where

, p(t), t=1, 2, 3…., T, where  is the mother wavelet (Kirikkaleli & Gokmenoglu, 2020). The transformed wavelet is indicated in the equation below by adding location and frequency.

is the mother wavelet (Kirikkaleli & Gokmenoglu, 2020). The transformed wavelet is indicated in the equation below by adding location and frequency.

(9)

(9)

The continuous wavelet function after adding p(t), which represents time series data, is depicted below:

(10)

(10)

Where k and f are determinants of time and frequency domains and they are represented by a modified p(t) equation with the coefficient. After adding the coefficient of to equation (10) above, equation (11) is generated:

(11)

(11)

This study utilizes the wavelet power spectrum (WPS), which enables us to capture the vulnerable frequencies and periods of the time series variables to obtain information about the political and financial vulnerability of the Balkan countries. The WPS function is shown below:

(12)

(12)

One of the major benefits of WPS is that the approach reveals causal linkage between the PR and FR variables in a combined time-frequency-based causality, which makes it more advantageous than the traditional causality and correlation tests. The equation below shows the squared wavelet coherence (Kirikkaleli, 2020).

(13)

(13)

Where C represents time and the smoothing process over time, and 0 ≤ R2 (k,f) ≤ 1. Variables are correlated when R2(k,f) is close to 1 and is depicted in red color. Similarly, when it gets close to zero, variables are not correlated and are depicted in blue color. Torrence & Compo’s (1998) strategy of examining differences in the wavelet coherence by employing deferrals in the wavering of two-time series is used to solve the challenge of R2(k,f), which does not provide insight into the negative and positive correlation. The equation below shows the wavelet coherence phase difference:

, (14)

, (14)

In the wavelet coherence analysis, an imaginary operator is represented by L and O for the real portion operator. When arrows point to the right (left) in the thick black area of the wavelet coherence analysis, variables are said to be positively (or negatively) correlated. Arrows that point up and down are another sign of causality (Cai et al., 2017). When arrows point left-up or right-down, it implies that the first variable is leading the second, and when they point left-down or right-up, it means the second variable is leading the first. Since the first variable is financial risk and the second is political risk, arrows pointing left-up or right-down indicate that financial risk leads to political risk, while arrows pointing left-down or right-up indicate the opposite. Political risk is leading when arrows point straight up and lagging when arrows point straight down.

3. Empirical Findings and Interpretations

3.1 Unit Roots Test Outcomes

The preliminary step was to prevent spurious regression, hence this study employs a single structural break unit root test of Zivot & Andrews (2002). Table 2 presents the result of Zivot Andrews’s unit root tests, which are analyzed categorically across all four Balkan countries. The Zivot-Andrews unit root results show that the PR and FR variables are integrated at both I(1) and I(0) and none of the variables were I(2) or higher.

Table 2: Summary of Unit Root Test outcomes.

|

Unit Root

|

Greece

|

Albania

|

Bulgaria

|

Romania

|

|

Technique

|

|

|

|

|

|

|

|

|

|

|

PR

|

FR

|

PR

|

FR

|

PR

|

FR

|

PR

|

FR

|

|

Zivot-Andrew

|

I (0)**

|

I (0)***

|

I (1)***

|

I (1) *

|

I (0)**

|

I(0)**

|

I(0)*

|

I(0)*

|

|

BreakPoint

|

(1993Q3)

|

(2010Q2)

|

(2002Q2)

|

(1996Q2)

|

(1994Q3)

|

(1998Q1)

|

(1999Q1)

|

(1999Q4)

|

|

|

|

|

|

|

|

|

|

|

Note: *, **, and *** denote statistically significant at the 10%, 5%, and 1% levels, respectively.

3.2. NARDL Estimations Test Outcomes

3.2.1. NARDL Estimations Test Outcomes for Greece

The next step in the risk modeling procedure is to ascertain the long- and short-term asymmetric effects of the PR and FR linkages between the countries. The paper rejects the null hypothesis of no co-integration between political risk and financial risk in Greece because, as illustrated in figure 3 below, the calculated t-statistic and f-statistic are greater than the critical values of those developed and postulated by Banerjee et al. (1998) and Pesaran et al., (2001) at 1% and 5% significant values, respectively. According to the calculated long-run coefficients, the political risk in Greece is statistically impacted by both positive and negative financial risk. The positive coefficient for the positive portion of financial risk will cause a rise in PR of 0.129%, while the positive coefficient for the negative portion of financial risk will cause a rise in PR of 0.028%. This indicates that any shock in financial risk, whether positive or negative, contributes to an increase in political risk in Greece. In the short run, the estimated coefficient shows that a positive or negative shock to financial risk positively correlates with political risk. Any positive or negative shock to financial risk increases political risk by 0.069% (0.067%). Summarily, both positive and negative financial shocks in Greece increase its positive political risk, both in the short and long term.

Table 3: NARDL Estimation for the Balkan Countries where Financial Risk is the Regressor.

Bulgaria Albania Greece

Long-Run Estimates

Regressors Coeff T-stat P-value Coeff T-stat P-value Coeff T-stat P-value

0.139 4.28 0.00 0.093 2.34 0.02 0.129 3.32 0.00

0.139 4.28 0.00 0.093 2.34 0.02 0.129 3.32 0.00

-0.055 1.16 0.25 0.155 4.33 0.00 0.028 0.51 0.60

-0.055 1.16 0.25 0.155 4.33 0.00 0.028 0.51 0.60

Short-Run Estimates

-0.015 -0.37 0.71 0.006 0.25 0.80 0.069 0.93 0.35

-0.015 -0.37 0.71 0.006 0.25 0.80 0.069 0.93 0.35

-0.027 -0.49 0.63 0.161 2.89 0.00 0.067 1.18 0.24

-0.027 -0.49 0.63 0.161 2.89 0.00 0.067 1.18 0.24

F-stat P-Value F-stat P-Value F-stat P-Value

Long-Run Asy 0.010 0.91 2.232 0.138 57.29 0.00

Short-Run Asy 0.545 0.46 1.001 0.319 0.550 0.46

The co-integration test statistics include Bulgaria (t BDM = -2.7757, F PSS = 4.0253), Albania (t_BDM = -5.3522, F_PSS = 6.5515), Romania (t_BDM = -2.7293, F_PSS = 2.0047), and Greece (t_BDM = -4.9555, F_PSS = 6.3306). The t-statistics' critical value is equivalent to -2.76, while the F-statistics' critical values are equal to 3.47, 4.01 and 5.17 at 1%, 5%, and 10%, respectively. Short-Run Asy = Short-Run Asymmetry and Long Run Asy = Long Run Asymmetry.

3.2.2. NARDL Estimations Test Outcomes for Bulgaria

With regards to Bulgaria, the null hypothesis is rejected also simply because the study's t-statistics (t BDM) is higher than the critical value using Banerjee et al., (1998) as a benchmark at a 5% significant level, indicating co-integration between the PR and FR variables in the country. The f- statistic exceeds Pesaran et al. (2001)'s the critical value by more than 1% at the 1% significant level. The study for the NARDL's estimated t-statistics and f-statistics (F PSS) shows co-integration between PR and FR, indicating that PR is linked to Bulgaria's FR.

The coefficients for the positive (negative) portions of financial risk indicate that over the long term, a positive (negative) shock to financial risk will cause an increase in the political risk of 0.139% and a decrease in political risk of (-0.055%), respectively. This study suggests that any positive shock to financial risk contributes to an increase in political risk, and any negative shock to financial risk contributes to a decrease in political risk in Bulgaria. In order words, every negative shock to Bulgaria's financial risk lowers the nation's long-term political risk. Moreover, any positive (negative) shock to Bulgaria's financial risk will, in the short run, cause a decrease in political risk of up to -0.015% (-0.027%), suggesting that any shock to financial risk, whether positive or negative, contributes to a short-term reduction in political risk in Bulgaria.

3.2.3. NARDL Estimations Test Outcomes for Albania

We adopt the alternative hypothesis because, in the case of Albania, the study's t-statistics (t BDM) is higher than the crucial value using Banerjee et al. (1998) as a benchmark at a 5% significant level. It indicates that Albania's political risk and financial risk indicators are co-integrated. Additionally, the f- statistics exceeds the Pesaran et al. (2001) 1% significant level crucial value. Therefore, the study for the NARDL's calculated t-statistics and f-statistics (F PSS) demonstrate a linkage between political risk and financial risk. In the long run, positive coefficients of financial risk demonstrate that a positive (negative) shock to financial risk has increased political risk by 0.093% (0.155%), which means that any positive ( (negative) shock to financial risk contributes to an increase in political risk in Albania. In the short term, a positive (negative) shock to financial risk also raises the political risk by 0.006% (0.161%), according to the positive coefficients for both the positive and negative sections of financial risk. In conclusion, any positive or negative shock in political risk plays a role in increasing Albania's financial risk in both the short and long run.

3.3. Wavelet Approach Test Outcomes

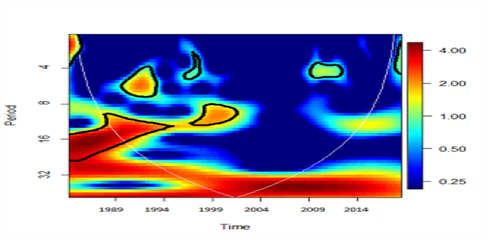

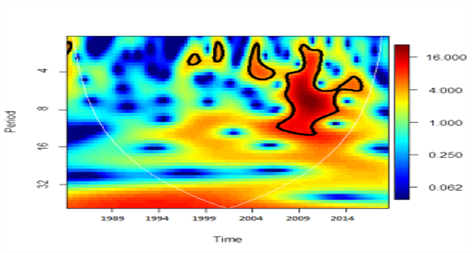

As in figure 1 below, the red color indicates the high political risk activities. In Greece, high political risk activities occurred from 1989 to 2000 in the medium –run (on a scale of 8-16). During this period, several political events took place, including (i) protests against the government's plan to curtail the president's authority, (ii) an internal crisis brought on by opposition to the Republic of Macedonia's flag and name, (iii) tension between Greece and Turkey over the Aegean Isles dispute and (iv) tension resulting from the killing of a British diplomat by a left-wing guerrilla group (BBC). Also, significant vulnerability is revealed from 1990 to 2002 in Albania in the long run (in the 16-32 scales). Some of the political events in Albania during this period include- (i) the conviction of corrupt politicians – Fatos Nano and Ramiz Alia, (ii) the Protest against the death of Azem Hajdari, (iii) internal conflicts from the succession of Pandeli Majko and (iv) fraud from general elections. More so, the result of Bulgaria shows that high political risk occurred from 1989 to 2005 in the medium run. The political events during this period include- (i) the collapse of the Bulgarian Socialist Party government in the face of mass demonstrations, (ii) the arrest of Todor for corruption, and (iii) elections as Zhan Videnov becomes prime minister. In addition, Romania's power spectrum indicates weak political risk vulnerability from 1989 to 1999 at different frequencies except from 1999 to 2003, and the political activities during this period include disputes resulting from the killing of Nicolae Ceausescu and his wife, ex-communist leadership protests, and miner riots, to name a few.

|

Greece

|

Albania

|

|

Bulgaria

|

Romania

|

Figure 1. Wavelet Power Spectrum for Political Risk.

Source: Author using Political Risk Group (2019) data

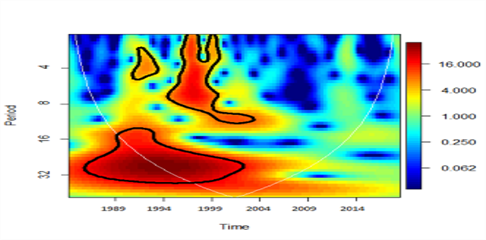

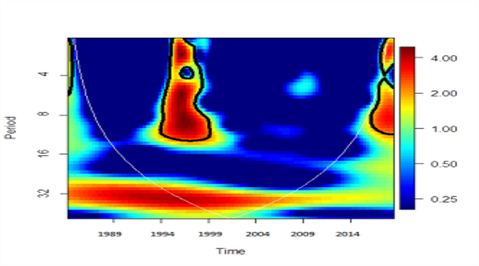

Figure 2 shows the wavelet power spectrum of financial risk across the four Balkan countries. As previously indicated, the x-axis represents the wavelet location in time, while the y-axis represents the wavelet period in years. As seen in the figure, Greece experienced significant short- and medium-term financial risk vulnerability from 2008 to 2014 (at different scales) and 2004 and 2001 (at the 2-4 scale). The sovereign debt crisis prompted more austerity measures in exchange for debt the European Union had sanctioned. More austerity measures were also agreed upon, with a 50% debt write-off from the EU. The worldwide financial crisis and Greece's sovereign debt crisis are, therefore, represented by the financial risk in Greece from 2008 to 2014. So, when the Greek parliament was debating EU treaties and policies, the country's finances collapsed due to the adverse impact of the world financial crisis and long-term trends in current account imbalances and budget deficits.

In addition, Albania indicates significant financial activities in the short- and medium-terms (at different frequencies) from 1997 to 1999; this represents the collapse of Albania's pyramid investment schemes. In contrast, Bulgaria's wavelet power spectrum from 1994 to 1999 is statistically significant in the medium- and long terms. The devaluation of the Bulgarian currency was a source of financial risk during this time. The financial risk was particularly susceptible in Romania between the 4-8 and 8-16 scales from 1999 to 2001. Therefore, whereas Greece's financial risk vulnerability is mainly in the '20s, it is dominant in the '90s in Bulgaria, Romania, and Albania. Any political risk shock, positive or negative, contributes to a rise in FR in Albania over the long and short run.

|

Greece

|

Albania

|

|

Bulgaria

|

Romania

|

Figure 2. Wavelet Power Spectrum for Financial Risk.

Source: Author using Political Risk Group (2019) data

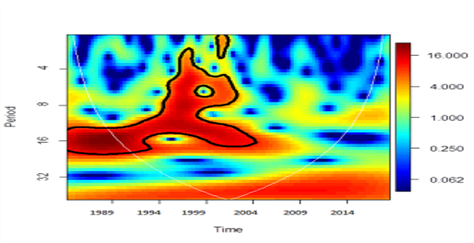

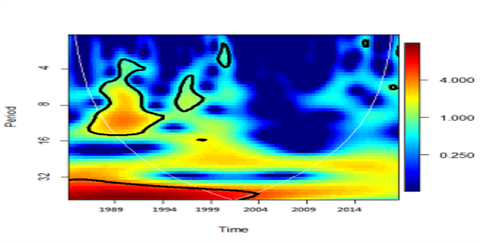

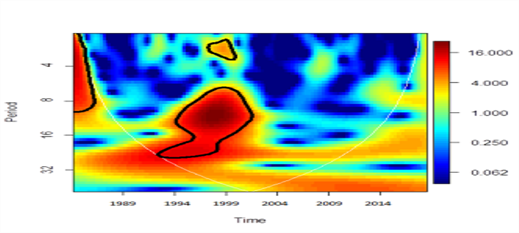

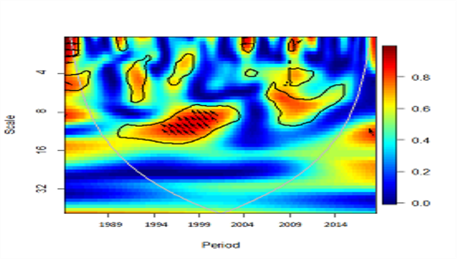

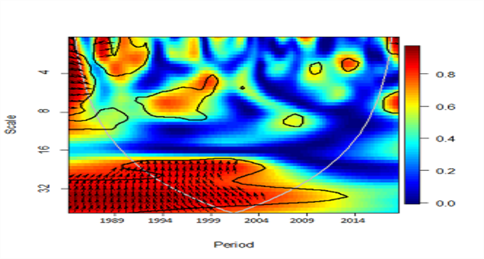

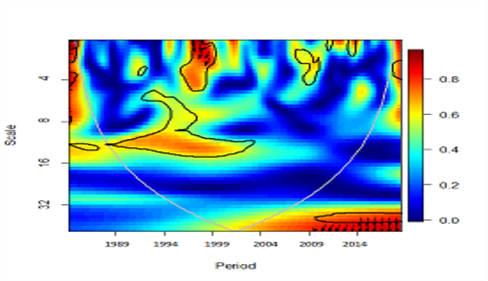

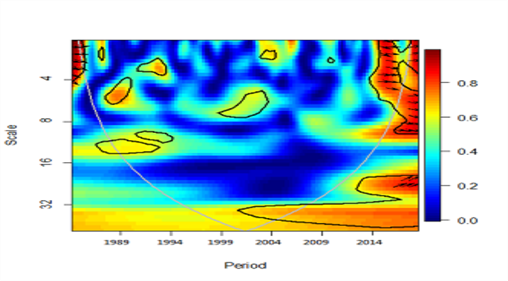

The wavelet coherence between PR and FR is shown in Figure 3 below; the couture lines represent wavelet squared coherence values of 0.0, 0.2, 0.4, 0.6, and 0.8. Curves with red colors and the black lines surrounding them are the more vulnerable regions. The arrows also depict co-movements between the two variables. In Greece, political risk and financial risk are statistically correlated. From 1995 to 2002, which corresponds to an eight-year cycle period, the primary region is in the medium-term between the 8 and 16 scales when FR is a good predictor of PR. This finding in Greece is consistent with research by (Pantzalis et al., 2000), which found that PR is a direct effect of FR. However, at high frequency, there was a negative correlation in 2004 and, in the short run, a positive correlation in 1988.

In contrast, lead-lag causality from PR to FR was shown in 2009. In the case of Albania, significant causality between 1991 and 2002 demonstrates that political risk leads to financial risk because the arrows between the 16 and 32 scales point directly upward, and a positive correlation between the two scales was seen in 1989 in the short run, in the 2 to 4 scales. Furthermore, a two-year cycle from 2003 to 2004 shows an opposite lead-lag association from financial to political risk. The 2009 global financial crisis had little impact on Albania since the country lacks standard financial markets, which can be considered a blessing in disguise.

Additionally, the main central region in Bulgaria is shown to have a highly significant coherence between 1996 and 1999. In the short run, changes in PR lead to FR on a scale of 2 to 4. The situation in Bulgaria is significantly different since, from 1996 to 1999, we saw that financial risk leads to political risk in the short run. Romania's most statistically significant area is the high-frequency region between the 2–4 and 4–8 scales, which has a positive connection between 2013 and 2015. More so, there was a positive correlation in 1988, which shows a positive association between PR and FR in the short run.

|

Greece

|

Albania

|

|

Bulgaria

|

Romania

|

Figure 3. Wavelet Coherence between Political Risk and Financial Risk.

Source: Author using Political Risk Group (2019) data.

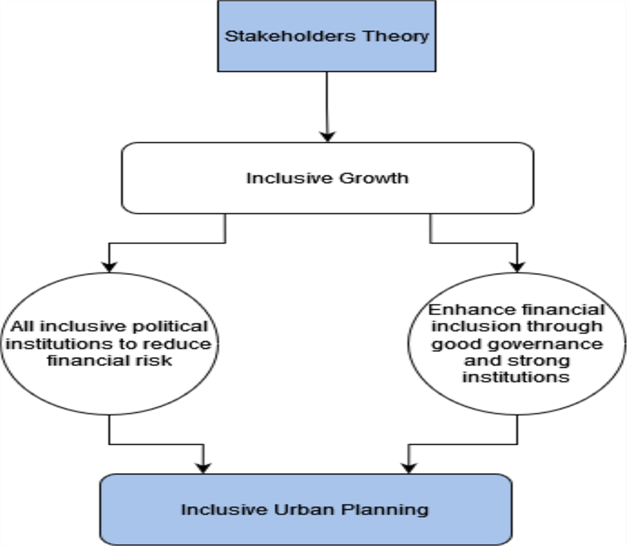

This study proposed a conceptual framework of inclusive growth to mitigate PR and FR in the countries, as shown in figure 4 below.

Figure 4. The figure proposed a conceptual framework for inclusive growth for countries.

Source: Author’s computation

Political institutions are essential for a country's success because strong political institutions determine good economic institutions. An individual's property rights are assigned to them by the constitutional state, which also guarantees them. The promise of property rights serves as the primary incentive for people and businesses to gather inputs for production and utilize them in manufacturing. When looking at inclusive growth from a political standpoint, it is important to have an impartial judiciary that will uphold law and order neutrality. Power should also not be concentrated within small individuals or elite groups. Better inclusive growth is facilitated by social capital, which includes public trust in leadership, the government, and civic involvement (Wilson, 1997). Political institutions are open to everyone, regardless of background, gender, or area. Inclusive political institutions' influence impacts a nation's income and production on economic processes like investment in factors of production (Porta et al., 2008).

By ensuring that all participants have access to the same level of services and opportunities as one another, inclusive urbanization aims to address difficulties with access to urban services and the equality of the socio-economic structure. Furthermore, effective political and financial institutions with the foresight of inclusive growth will ensure adequate decision-making. Inclusive urbanization that embraces well plan housing policy and less restrictive land use regulations where all stakeholders- such as women, children, migrant workers, and refugees, are taken into account can enhance better livelihood for all.

4. Conclusion and Recommendations

In order to assess the asymmetry and time-frequency relationship between political risk and financial risk in the Balkan countries, the paper used a quarterly dataset spanning from 1984Q3 to 2018Q4. The dataset in this study is broken down into time-frequency space using a wavelet, which makes it easy to determine the short-, medium-, and long-term interactions between the two variables. Our NARDL findings show an asymmetric relationship between political risk and financial risk in Albania, Greece, and Bulgaria, except Romania, which lacks co-integration. Additionally, our results from the wavelet coherence analysis demonstrated that political risk in Albania and Bulgaria is a good predictor of financial risk. While financial risk drives political risk in Greece, Romania's result shows a positive correlation between political risk and financial risk at different frequencies. Furthermore, in terms of the linkage between PR and FR, our findings support those of Pástor & Veronesi (2013) and Białkowski et al. (2008), who show how political risk affects financial development.

The study also brings to bare recommendations for urban planning development in the Balkan countries. First, we recommend that the Balkan countries' urbanization development becomes mature. The government of Albania, Bulgaria, Romania and Greece should focus on how to reduce political and financial instability to improve urbanization, which will consequently help urban planners develop cities, towns or regional planning. In addition, the government should enact urban planning laws that are amenable to the dynamics in the political and financial situations, as authoritarian leadership can either make static urban policies or slow down urban planning processes. Furthermore, reducing corruption can reduce the bureaucratic processes involved in implementing and executing urban planning policies. Hence, good governance via a good leadership style, effective handing over during regime change and a stable financial regime can enhance an effective urban planning system. Finally, to enhance the effective financial sector, the study recommends long-run financial policy reforms, increase public trust in the countries’ financial system and credible all-inclusive political parties to attain all-inclusive financial systems. Future studies should consider other macroeconomic variables in the estimation of NARDL co-integration in a country-specific analysis.

Funding

This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Conflicts of interest

The Author(s) declares(s) that there is no conflict of interest.

Data availability statement

The data that supports the findings of this study can be purchased directly from Political Risk Service Group or available from the authors upon reasonable request

Ethics statements

Studies involving animal subjects: No animal studies are presented in this manuscript.

Studies involving human subjects: No human studies are presented in this manuscript.

Inclusion of identifiable human data: No potentially identifiable human images or data is presented in this study.

CRediT author statement

Conceptualization: The wavelet concept is by D. K. while the NARDL concept in the paper is by Sadat Shuaibu. Data curation: D. K. bought data from the Public Risk Service Group. Formal Analysis: Sadat used stata for the NARDL and did the analysis while D. K. used the R-software for wavelet analysis. Funding acquisition- This research did not receive any grant from funding agencies. Methodology- NARDL models are made available by S. M. S. while wavelet models are by D. K. Project administration: Coordination responsibility by D. K. Resources: Analysis tool, R-software provided by D. K. while stata was made available by S. M. S. Software: by S. M. S. and D. K. Supervision: Oversight responsibility for the research activity was done by D. K. Validation- Validated by S. M. S. Visualization- S. M. S. Roles/writing: S. M. S. wrote the draft. All authors have read and agreed to the published version of the manuscript.

References

Alesina, A., & Tabellini, G. (1989). External debt, capital flight and political risk. Journal of International Economics, 27(3–4), 199–220. https://doi.org/10.1016/0022-1996(89)90052-4

Arcand, J. L., Berkes, E., & Panizza, U. (2015). Too much finance? Journal of Economic Growth, 20(2), 105–148. https://doi.org/10.1007/s10887-015-9115-2

Ashraf, H., & Prentice, R. (2019). Beyond factory safety: labor unions, militant protest, and the accelerated ambitions of Bangladesh’s export garment industry. Dialectical Anthropology, 43(1), 93–107. https://doi.org/10.1007/s10624-018-9539-0

Banerjee, A., Dolado, J., & Mestre, R. (1998). Error-correction Mechanism Tests for Cointegration in a Single-equation Framework. Journal of Time Series Analysis, 19(3), 267–283. https://doi.org/10.1111/1467-9892.00091

Barro, R. J. (1991) . A cross-country study of growth, saving, and government. In National saving and economic performance. University of Chicago Press, 271–304.

Benedek, J. (2006). Urban policy and urbanization in the transition Romania. Romanian Review of Regional Studies, 2(1), 51–64. https://doi.org/10.1016/j.cities.2010.02.002

Berdiev, A. N., Kim, Y., & Chang, C. P. (2012). The political economy of exchange rate regimes in developed and developing countries. European Journal of Political Economy, 28(1), 38–53. https://doi.org/10.1016/j.ejpoleco.2011.06.007

Białkowski, J., Gottschalk, K., & Wisniewski, T. P. (2008). Stock market volatility around national elections. Journal of Banking & Finance, 32(9), 1941–1953. https://doi.org/10.1016/j.jbankfin.2007.12.021

Bredin, D., Conlon, T., & Potì, V. (2015). Does gold glitter in the long run? Gold as a hedge and haven across time and investment horizons. International Review of Financial Analysis, 41, 320–328. https://doi.org/10.1016/j.irfa.2015.01.010

Butkiewicz, J. L., & Yanikkaya, H. (2006). Institutional quality and economic growth: Maintenance of the rule of law or democratic institutions, or both? Economic Modelling, 23(4), 648–661. https://doi.org/10.1016/j.econmod.2006.03.004

Cai, X. J., Tian, S., Yuan, N., & Hamori, S. (2017). Interdependence between oil and East Asian stock markets: Evidence from wavelet coherence analysis. Journal of International Financial Markets, Institutions and Money, 48, 206–223. https://doi.org/10.1016/j.intfin.2017.02.001

Cassette, A., & Farvaque, E. (2014). Are elections debt breaks? Evidence from French municipalities. Economics Letters, 122(2), 314–316. https://doi.org/10.1016/j.econlet.2013.12.022

Chan, Y., & John Wei, K. C. (1996). Political risk and stock price volatility: The case of Hong Kong. Pacific-Basin Finance Journal, 4(2–3), 259–275. https://doi.org/10.1016/0927-538X(96)00014-5

Charfeddine, L., & al Refai, H. (2019). Political tensions, stock market dependence and volatility spillover: Evidence from the recent intra-GCC crises. The North American Journal of Economics and Finance, 50, 101032. https://doi.org/10.1016/j.najef.2019.101032

Cutler, D., Poterba, J., & Summers, L. (1988). What Moves Stock Prices? https://doi.org/10.3386/w2538

Delavallade, C. (2006). Corruption and distribution of public spending in developing countries. Journal of Economics and Finance, 30(2), 222–239. https://doi.org/10.1007/BF02761488

Funke, M., Schularick, M., & Trebesch, C. (2016). Going to extremes: Politics after financial crises, 1870–2014. European Economic Review, 88, 227–260. https://doi.org/10.1016/j.euroecorev.2016.03.006

González-Fernández, M. , & González-Velasco, C. (2014). Shadow economy, corruption and public debt in Spain. Journal of Policy Modeling, 36(6), 1101–1117.

Goupillaud, P., Grossmann, A., & Morlet, J. (1984). Cycle-octave and related transforms in seismic signal analysis. Geoexploration, 23(1), 85–102. https://doi.org/10.1016/0016-7142(84)90025-5

GYÖNGYÖSI, G., & VERNER, E. (2022). Financial Crisis, Creditor‐Debtor Conflict, and Populism. The Journal of Finance, 77(4), 2471–2523. https://doi.org/10.1111/jofi.13138

Hacker, J. S. (2019). The great risk shift: The new economic insecurity and the decline of the American dream. Oxford University Press.

Hillier, D., & Loncan, T. (2019). Political uncertainty and Stock returns: Evidence from the Brazilian Political Crisis. Pacific-Basin Finance Journal, 54, 1–12. https://doi.org/10.1016/j.pacfin.2019.01.004

Howell, L. D. (2011). International Country Risk Guide Methodology. The PRS Group.

Humphrey, C., & Michaelowa, K. (2019). China in Africa: Competition for traditional development finance institutions? World Development, pp. 120, 15–28. https://doi.org/10.1016/j.worlddev.2019.03.014

Kirikkaleli, D. (2016). Interlinkage Between Economic, Financial, and Political Risks in the Balkan Countries: Evidence from a Panel Cointegration. Eastern European Economics, 54(3), 208–227. https://doi.org/10.1080/00128775.2016.1168704

Kirikkaleli, D. (2020). Does political risk matter for economic and financial risks in Venezuela? Journal of Economic Structures, 9(1), 3. https://doi.org/10.1186/s40008-020-0188-5

Kirikkaleli, D., & Gokmenoglu, K. K. (2020). Sovereign credit and economic risk in Turkey: Empirical evidence from a wavelet coherence approach. Borsa Istanbul Review, 20(2), 144–152. https://doi.org/10.1016/j.bir.2019.06.003

Lerch, M. (2014). The Role of Migration in the Urban Transition: A Demonstration From Albania. Demography, 51(4), 1527–1550. https://doi.org/10.1007/s13524-014-0315-8

Li, J., & Born, J. A. (2006). PRESIDENTIAL ELECTION UNCERTAINTY AND COMMON STOCK RETURNS IN THE UNITED STATES. Journal of Financial Research, 29(4), 609–622. https://doi.org/10.1111/j.1475-6803.2006.00197.x

Mauro, P. (1998). Corruption and the composition of government expenditure. Journal of Public Economics, 69(2), 263–279. https://doi.org/10.1016/S0047-2727(98)00025-5

Pantzalis, C., Stangeland, D. A., & Turtle, H. J. (2000). Political elections and the resolution of uncertainty: The international evidence. Journal of Banking & Finance, 24(10), 1575–1604. https://doi.org/10.1016/S0378-4266(99)00093-X

Pástor, Ľ., & Veronesi, P. (2013). Political uncertainty and risk premia. Journal of Financial Economics, 110(3), 520–545. https://doi.org/10.1016/j.jfineco.2013.08.007

Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

Pojani, D. (2009). Urbanization of Post-communist Albania: Economic, Social, and Environmental Challenges. Debatte: Journal of Contemporary Central and Eastern Europe, 17(1), 85–97. https://doi.org/10.1080/09651560902778394

Porta, R. la, Lopez-de-Silanes, F., & Shleifer, A. (2008). The Economic Consequences of Legal Origins. Journal of Economic Literature, 46(2), 285–332. https://doi.org/10.1257/jel.46.2.285

Roberts, M., & Townshend, T. G. (2017). Urban design in an age of recession. Journal of Urban Design, 22(2), 133–136. https://doi.org/10.1080/13574809.2017.1295787

Scrivens, K., & Smith, C. (2013). Four Interpretations of Social Capital: An Agenda for Measurement. OECD Statistics Working Papers No. 2013/06, OECD Publishing, Paris.

Shahbaz, M., Nasir, M. A., Hille, E., & Mahalik, M. K. (2020). UK’s net-zero carbon emissions target: Investigating the potential role of economic growth, financial development, and R&D expenditures based on historical data (1870–2017). Technological Forecasting and Social Change, 161, 120255. https://doi.org/10.1016/j.techfore.2020.120255

Shahbaz, M., Tiwari, A. K., & Tahir, M. I. (2015). Analyzing the time-frequency relationship between oil price and exchange rate in Pakistan through wavelets. Journal of Applied Statistics, 42(4), 690–704. https://doi.org/10.1080/02664763.2014.980784

Siokis, F., & Kapopoulos, P. (2003). Electoral management, political risk and exchange rate dynamics: the Greek experience. Applied Financial Economics, 13(4), 279–285. https://doi.org/10.1080/13504850210128839

Smales, L. A. (2015). Better the devil you know: The influence of political incumbency on Australian financial market uncertainty. Research in International Business and Finance, 33, 59–74. https://doi.org/10.1016/j.ribaf.2014.06.002

Suraj, D. (2015). Global Financial Crisis of 2007: The Case of Albania. Mediterranean Journal of Social Sciences. https://doi.org/10.5901/mjss.2015.v6n4p130

Torrence, C., & Compo, G. P. (1998). A Practical Guide to Wavelet Analysis. Bulletin of the American Meteorological Society, 79(1), 61–78. https://doi.org/10.1175/1520-0477(1998)079<0061:APGTWA>2.0.CO;2

Wilson, P.A.(1997) Building Social Capital: A Learning Agenda for the Twenty-First Century. Urban Studies, 34(5-6), 745–760. https://doi.org/10.1080/0042098975808

Zivot, E., & Andrews, D. W. K. (2002). Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics, 20(1), 25–44. https://doi.org/10.1198/073500102753410372